Being

the second most populous country in the world, India has enormous potential to

become the global power house. Even though we have come a long way, the bigger

hurdles are yet to overcome. One of them is poverty. Amartya Sen once said

"Poverty is not just lack of money.

It is not having the capability to realize one's full potential as a human

being". The government has been trying to address the issue of poverty

since independence, but still one third of our population is below the poverty

line. This poses a question - Is addressing poverty is that difficult? Or are

we addressing it in a wrong way?

The

conventional approach of government towards addressing the issue of poverty is

through subsidies and public distribution system.

But

the majority of the spending gets absorbed into our complex bureaucratic system

through corruption, red-tapism, and implementation delays. Transforming the bureaucratic

regime is a cumbersome process. Is there any other alternate way where we can

address the issue of poverty and achieve the sustainable development of our

nation?

The

one word solution is "Inclusive

growth through financial inclusion"

Inclusive

growth can be defined as providing equitable opportunities and a level playing

field to all citizens thereby sharing the benefits of economic growth even

handedly. Financial inclusion is the stepping stone towards achieving inclusive

growth.

Leveraging the hidden potential of the

bottom of the pyramid section of our nation

As

per the Rangarajan Committee report on financial inclusion, financial inclusion

can be defined as “the process of

ensuring access to financial services and timely and adequate credit where

needed by vulnerable groups such as weaker sections and low income groups at an

affordable cost”. In India, the concept of financial inclusion was

introduced a decade back by Mr. K C Chakrabarty. Mangalam, a small village from

the state of Tamil Nadu was the first to be brought under the financial

inclusion plan and subsequently banking services were provided to all the

villagers.

Financial

inclusion can act as a stepping stone towards inclusive growth because of the

following reasons.

1. It

provides a level playing field where one can access the formal financial system

for borrowing and lending.

2. The

cost of borrowing will reduce drastically and as a result economic growth and

prosperity will be achieved.

3. It

promotes the saving habits of people thereby increasing the capital formation

of the nation.

4. It

will help in increased transparency, elimination of middlemen and facilitate

huge inflow of money into the formal banking system.

5. It

will act as an impetus in eliminating poverty, unemployment and income

inequalities in the long run.

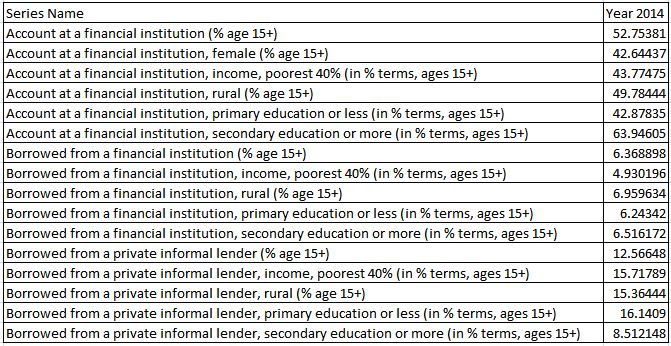

|

Figure 01 - Source

of data – World Bank, The global Findex database 2014

|

Key observations from the report

Nearly

half of the population in India still does not have access to formal financial

institution. The situation is even bleaker when it comes to females and the poorest

section of the society.

As

per the policy research working paper published by World Bank, less than 5

percent of adults around the world reported borrowing from a private informal

lender. But in India, the percentage of borrowing from private informal lender is

a whopping 12.56%. The percentage of informal borrowing increases when it comes

to rural areas (15.36%) and people without having primary education (16.14%).

Education

level positively influences people in taking decisions. Almost 64 percent of

people who have completed secondary education have an account at a financial

institution and only 8.51% of people who possess secondary education or more

borrowed from a private informal lender.

From

these figures it is evident that the current situation is not so encouraging.

What have we done so far? -

Transformation in the financial services

The

recent announcement from the central bank giving fresh banking licenses almost

after a decade to two entities (IDFC and Bandhan Finance) with a strict rural

focus can be seen as a welcome move. At the same time the introduction of

payment banks, small savings banks, white label ATMs and Digital Banking are

going to act as stimulants. Another major transformation can be achieved

through JAM Trinity

JAM

trinity refers to Jan Dhan Yojana, Aadhar and Mobile. This is going to be one

of the biggest path-breaking reforms, if implemented effectively and will act

as a pillar in achieving financial inclusion and inclusive development. It can

deliver the subsidy and other benefits to people directly thereby eliminating

the inefficient distribution of subsidies.

Challenges & Road ahead

It

is laudable that the government has already taken significant steps in

achieving financial inclusion. But there are several challenges also.

As per the latest

financial stability report from RBI, credit growth of scheduled commercial

banks (SCB) is at 9.7 percent and the deposits growth is at 12.9 percent which

is way below compared to past time. At the same time the gross NPAs of SCBs is

at 4.6 percent. These problems can have adverse impacts on achieving equality

in credit disbursements and government should formulate viable solutions to

tackle these issues.

|

| Figure 02 – Credit growth & Deposit growth Source – Financial Stability Report, RBI |

Under

Pradhan Mantri Jan-Dhan Yojana, we have opened 18.47 crores of accounts (11.21

crores in rural areas, as on 23-09-2015). But the success of this scheme will

depend on how often people make transactions using these accounts. This is

extremely important considering the fact that India has a dormancy rate of 43

percent and accounts for about 195 million of the 460 million dormant accounts

around the world. As per the latest statistics, around 41.31 percent of the

accounts which is opened under PMJDY scheme have zero balance. Even though we

have witnessed a dramatic reduction in the zero balance accounts over the last

year (Refer Figure 03), the government should work more in order to bring all

the people under the umbrella of the formal financial system.

Achieving

financial inclusion by transforming the financial services is the best way to

make people competitive across all the sections of society and thereby

achieving inclusive development. Of course this will take time and we should

not depend on short term fixes. As the honorable governor of the RBI, Raghuram

Rajan pointed out “We have to have the

discipline to stick to our strategy of building the necessary institutions and

creating a new path of sustainable growth where Jugaad is no longer needed. For

this, what we need is the understanding and cooperation, not impatience and

pressure for quick impossible fixes. Only then can we realize our true

potential as a nation.”

Regards,

Harikrishnan

Views are personal

References